Artificial intelligence has driven one of the strongest technology rallies in recent years, with semiconductor companies supplying data centers and AI infrastructure leading the charge. Now, investors are looking for the next sector to benefit from the AI buildout, and Nvidia is signaling where it believes the next major growth opportunity lies: robotics and physical AI.

CEO Jensen Huang has repeatedly described robotics as the company's next long-term growth engine, calling humanoid robots a “multitrillion-dollar economic opportunity.” While robotics remains an early-stage market, Nvidia is steadily expanding beyond AI chips by building the software, computing platform, and development tools that could underpin future autonomous machines. The strategy suggests that the next phase of the AI boom may extend well beyond data centers into factories, warehouses, and industrial automation.

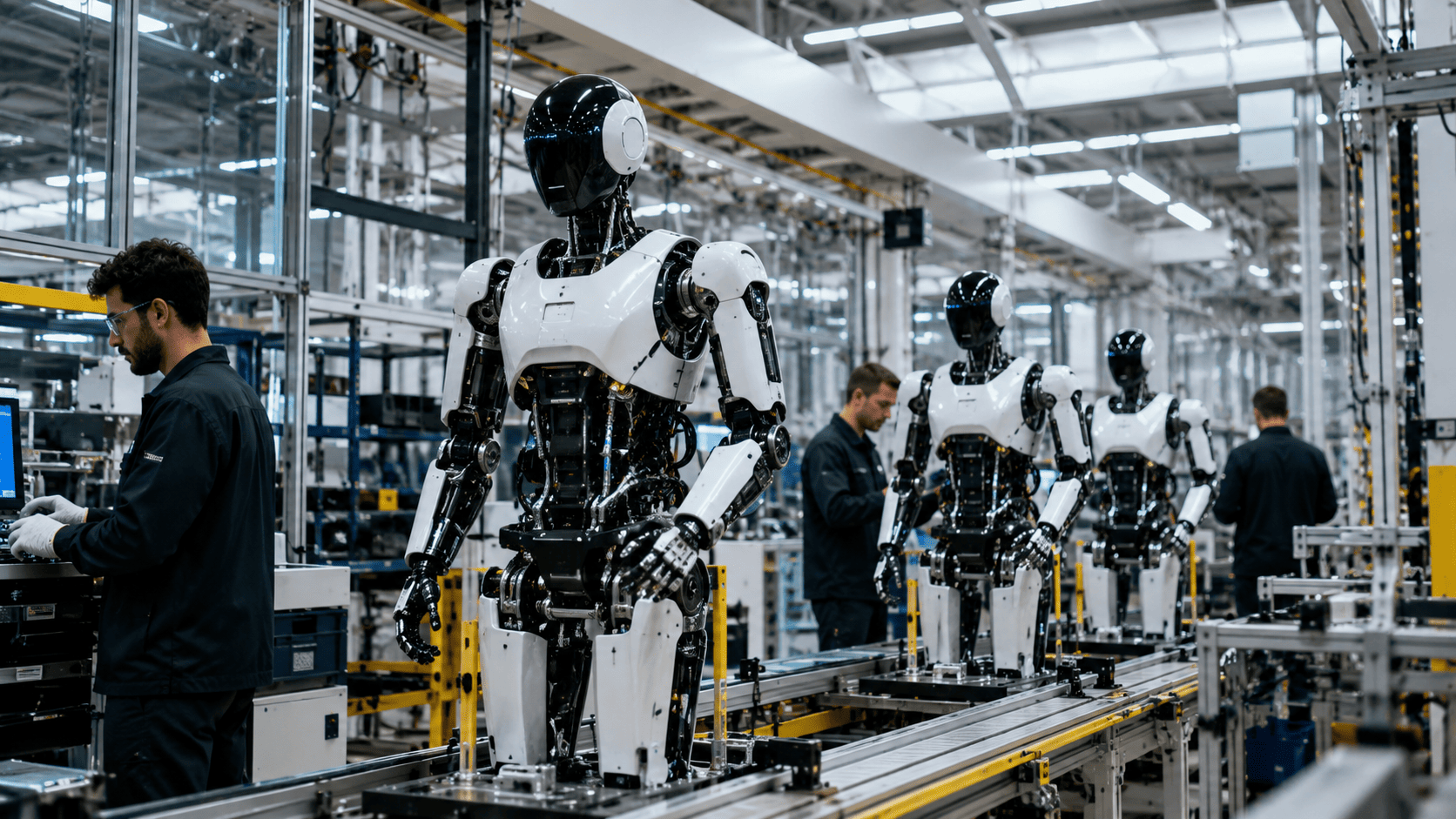

Nvidia Builds the Platform, Not the Robot

Rather than manufacturing humanoid robots itself, Nvidia is positioning its technology as the operating layer powering them. The company recently introduced its Halos for Robotics safety stack while continuing to expand its Isaac GR00T AI models, Jetson Thor computing platform, and Omniverse simulation software. Earlier this week, Nvidia unveiled its first integrated robotics system designed for researchers, combining Chinese robotics company Unitree's nearly six-foot-tall H2 humanoid robot with Nvidia's Jetson Thor hardware, powered by the company's Blackwell GPU architecture. The system also incorporates Nvidia's Isaac GR00T AI models, simulation software, and mechanical hands produced by Singapore-based Sharpa.

“Today, we’re announcing the Nvidia Isaac Root, a reference humanoid robot, all fully integrated, 25 degrees of freedom on that on each hand made by Sharpa, 31 degrees of freedom on the robot, six feet 150 pounds, just like me,” Huang said during a keynote speech in Taipei in June. “This platform runs the new Thor, and our entire software stack, data generation stack, data simulation stack, the runtime, all integrated into a robot that is designed for everyone to use.” The platform will initially be used by institutions including Stanford Robotics Center, ETH Zurich, Ai2, and the University of California San Diego.

Industrial Suppliers May Benefit Before Humanoids

Although Huang has pointed to robotics as a major long-term opportunity, humanoid robots currently contribute only a small portion of Nvidia's business. The company generated $215.9 billion in fiscal 2026 revenue, with its data center business accounting for $193.7 billion. Automotive and robotics together generated approximately $2.3 billion, with most of that coming from autonomous driving and factory automation rather than humanoid robots. That has shifted investor attention toward suppliers already participating in industrial automation.

According to consultancy McKinsey, actuators account for 40% to 60% of a humanoid robot's bill of materials, while sensing represents 10% to 20% and computing contributes roughly 10% to 15%. Those economics have increased investor interest in companies supplying motors, actuators, sensors, power systems, and factory automation. One example emerged in May, when Germany's Schaeffler agreed to deploy up to 2,000 humanoid robots from UK startup Humanoid across its manufacturing plants by 2032. The agreement also made Schaeffler the preferred supplier for more than half of Humanoid's actuator demand through 2031.

Other industrial automation companies integrating Nvidia technologies include Fanuc, ABB, Yaskawa Electric, and Kuka, which are incorporating Nvidia's Omniverse and Jetson platforms into factory automation and virtual commissioning tools. Several established industrial and technology companies are positioned across those parts of the robotics value chain. Teradyne owns Universal Robots and Mobile Industrial Robots, with its robotics division reporting four consecutive quarters of revenue growth. Rockwell Automation continues to benefit from rising demand for industrial automation, including autonomous mobile robots used in automotive, food and beverage, home care, and data center applications.

Tesla is pursuing its own humanoid robot strategy through Optimus while expanding investments in autonomous driving technologies. CEO Elon Musk has previously described robotics as a major long-term growth opportunity for the company, although commercial deployment of Optimus remains in its early stages. Competition is also expanding beyond Nvidia's ecosystem. Qualcomm has introduced its Dragonwing IQ10 processor targeting humanoid robots and is working with robotics developers including Figure Technology Solutions and Neura Robotics.

Robotics Market Continues to Expand Despite Challenges

The broader industrial robotics market is already growing even as humanoid robots remain in the early stages of commercialization. The International Federation of Robotics reported 542,000 industrial robot installations worldwide during 2024, marking the fourth consecutive year with more than 500,000 deployments. China accounted for 54% of installations, while South Korea ranked as the fourth-largest market. Meanwhile, GlobalData projects the robotics industry will expand from $76 billion in 2023 to over $200 billion by 2030.

For investors, the key takeaway is that while humanoid robots may take years to scale, the industrial automation and robotics supply chain is already benefiting from AI's expansion beyond data centers. Companies providing actuators, sensors, motors, and factory automation systems are well-positioned to capture growth as Nvidia and others push robotics into the mainstream. As Nvidia dips 0.75% as robotics push and partner stocks rally, the market is beginning to price in this next wave. Meanwhile, Nvidia lags chip rally as smart money rotates to memory, custom silicon, suggesting that the AI boom is broadening beyond the chipmaker itself.

This article is for informational purposes only and does not constitute financial advice.