As the second-quarter earnings season gains momentum, Morgan Stanley has singled out three stocks that it believes are positioned to deliver strong results: GE Vernova (NYSE:GEV), Lam Research (NASDAQ:LRCX), and United Airlines (NASDAQ:UAL). The investment bank's analysts point to robust demand drivers and favorable industry trends that could propel these companies past market expectations.

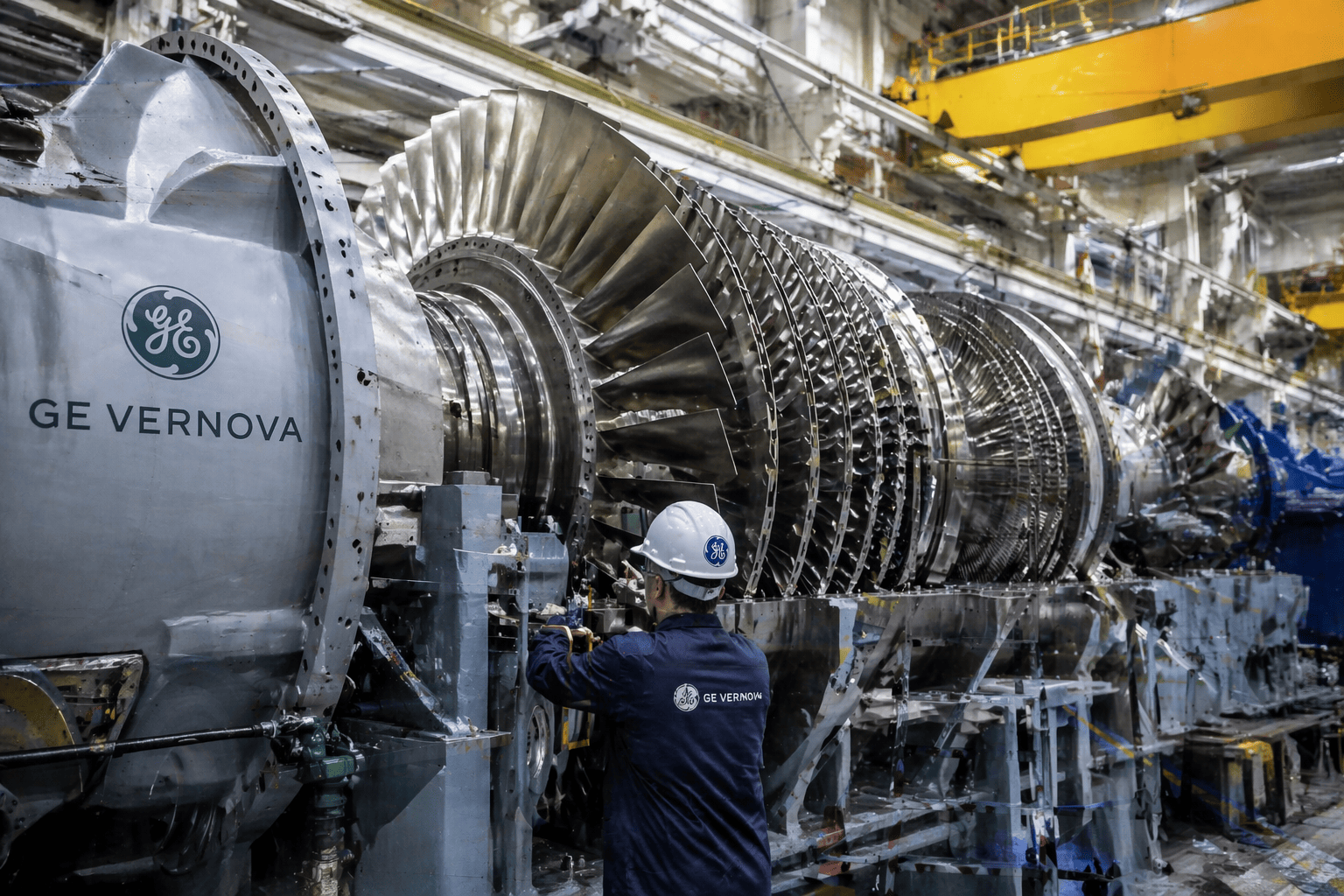

GE Vernova: Powering the AI Boom

GE Vernova has surged 61% year-to-date and nearly doubled over the past 12 months, fueled by rising demand for power equipment tied to the artificial intelligence boom. Despite a recent pullback from its all-time high, Morgan Stanley expects the company to rebound following its July 22 earnings report. Analysts anticipate stronger-than-expected results, supported by new gas turbine contracts. Management has indicated that gas turbine reservations are sold out through 2030, underscoring sustained demand.

Morgan Stanley's Michael Wilson noted, "Capex is broadening beyond data centers and reshoring progress suggests the U.S. industrial economy may be entering a sustained growth cycle as international production becomes more expensive than domestic." The average analyst target for GEV stock stands at $1,089, slightly above its current price of $1,067, with Bernstein setting a target of $1,206 and Jefferies recently lowering its target to $1,210.

United Airlines: Pricing Power and Fuel Cost Dynamics

United Airlines shares have risen 7% this year and 43% from their 2024 low, driven by a temporary ceasefire between the U.S. and Iran that lowered jet fuel prices. However, renewed hostilities have pushed oil prices above $80 per barrel, raising fuel costs. Despite this, Morgan Stanley remains bullish, citing healthy demand and pricing power. The bank wrote, "Airline demand and booking intent remain healthy, with seven consecutive price increases absorbed without demand destruction."

Analysts from Susquehanna, Cowen, Goldman Sachs, BMO, and Bernstein have raised their price targets for United Airlines this month, reflecting optimism about the carrier's forward guidance and ability to manage fuel costs.

Lam Research: AI Demand and Valuation Concerns

Lam Research, a semiconductor equipment maker, has seen its stock more than double this year before a 20% decline from its June record high of $437 to around $346. Morgan Stanley expects the company to report better-than-expected revenue and earnings, with potential for further earnings per share growth. The bank stated, "AI demand remains robust with rising token prices and continued strength across the ecosystem despite recent market pullbacks. New equipment orders are improving."

However, valuation remains a concern, with Lam Research trading at a forward price-to-earnings ratio of 62, significantly higher than peers like Nvidia, Micron, and SanDisk. Despite this, analysts remain bullish: Stifel raised its target from $325 to $425, Needham from $300 to $390, and others from Mizuho, Susquehanna, and Cantor Fitzgerald have also boosted their targets.

For context, the broader chip sector has faced headwinds from geopolitical tensions, as seen in recent market moves. The chip stocks plunge amid U.S.-Iran conflict highlights the risks to helium supply and the AI boom, while energy stocks surge on oil price rebounds. Investors should weigh these dynamics when evaluating Lam Research's prospects.

Morgan Stanley's picks reflect a broader theme of capital expenditure expansion and AI-driven demand, though each stock carries unique risks. GE Vernova benefits from industrial growth, United Airlines from pricing power, and Lam Research from semiconductor equipment demand. As earnings season unfolds, these names will be closely watched for confirmation of the bank's thesis.

This article is for informational purposes only and does not constitute financial advice.